[original need to be reprinted] A "wonder soldier" of Japanese semiconductors

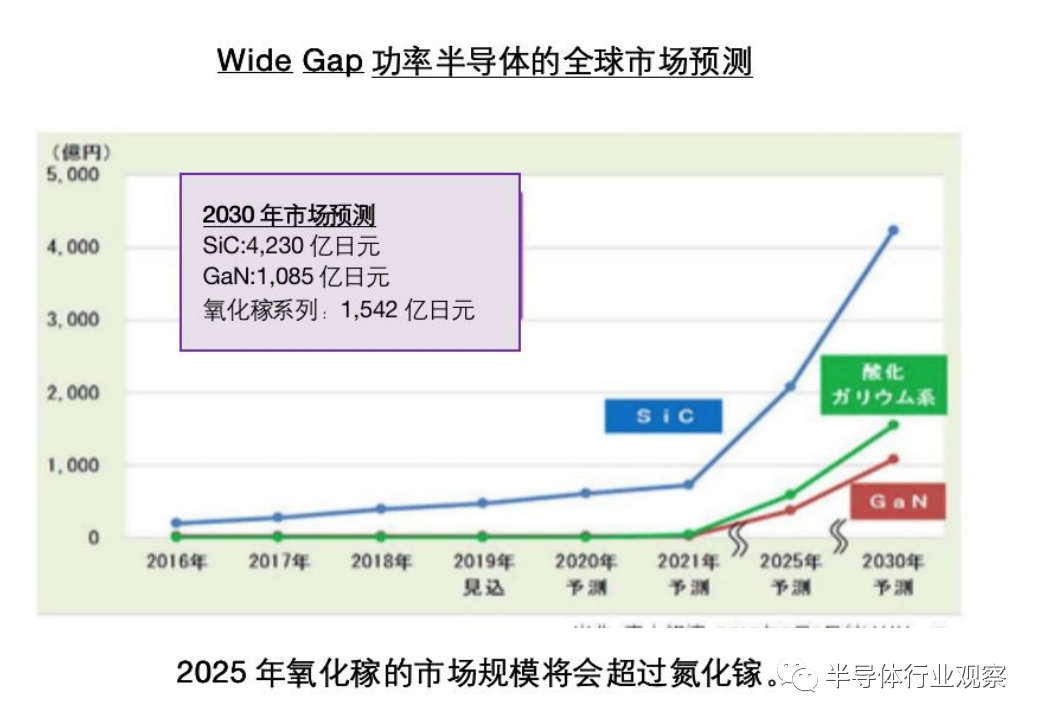

According to the global market forecast of WideGap power semiconductor components released by the market research company Fuji economy on June 5, 2019, the market size of gallium oxide power components will reach 154.2 billion yen and about 9.276 billion yuan in 2030, which is larger than that of gallium nitride power components of 108.5 billion yen, or about 6.51 billion yuan.

Toshiba and Fuji Motor will invest a total of 200 billion yen ($1.9 billion) to increase the production of energy-efficient chips for electric vehicles to adapt to the sharp shift from governments around the world to electric cars and trucks, the Nikkei reported.As we all know, in recent years, with the rapid development of consumer electronics, new energy vehicles, photovoltaic wind power and other downstream fields, power semiconductors have become the focus of global attention. According to the data, the power semiconductor market is expected to grow at a rate of 6% a year. Affected by this advantage, on the one hand, global power semiconductor manufacturers will strengthen their own strength by strengthening internal research and development to expand production; on the other hand, mergers and acquisitions have also become another important means for manufacturers to check and fill gaps.And Japanese manufacturers are undoubtedly an important force in this market.

Dazzling Japanese manufacturers

For many years, Japan has spared no effort in developing power semiconductors. According to the latest Japanese media reports, the Ministry of economy, Trade and Industry (METI) is preparing to provide financial support to private enterprises and universities dedicated to developing a new generation of low-energy semiconductor material gallium oxide. METI will set aside about US $20.3 million for next year and is expected to invest more than US $85.6 million in the next five years.

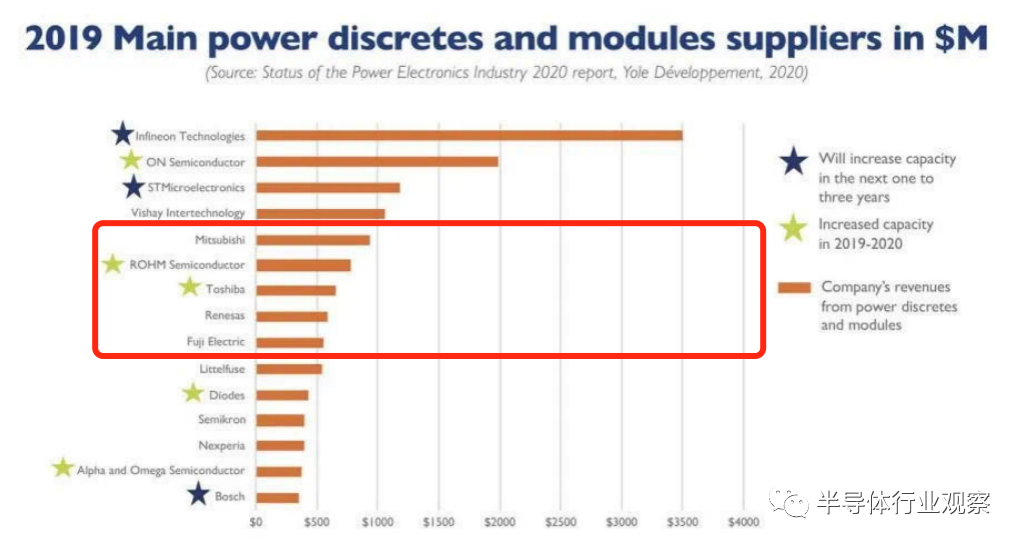

Driven by the pursuit of technology and capital, Japan has always had a strong strength in the field of power semiconductors. It is reported that at present, the world's power semiconductor devices are mainly provided by Europe, the United States, and Japan. With advanced technology and manufacturing technology, as well as leading quality management systems, they occupy about 60% of the global market share.Japanese companies Mitsubishi Electric (Mitsubishi), ROHM (Rom), Toshiba (Toshiba), Renesa Electronics (Renesas) and Fuji Motor (Fuji Electric) ranked among the top five to nine in the power semiconductor market (discrete components and modules) in 2019.Sales of manufacturers in the power semiconductor market (discrete components and modules) in 2019Recently, according to relevant reports, the Ministry of economy, Trade and Industry of Japan expects to stop selling new gasoline cars in Japan in the mid-2030s, selling only hybrid and pure electric models, and by 2050, the entire life cycle of cars from manufacturing to disposal and recycling will be carbon neutral.At present, the Japanese government is planning to introduce a preferential tax system on products that help save energy, such as batteries and power semiconductors. It is worth noting that the expansion of these daily factories is expected to alleviate the shortage of power semiconductors in Chinese vehicle enterprises.Under the Japanese government's incentive policy for new energy vehicles, Japanese manufacturers are actively expanding production and preparing for war.

Japanese manufacturers who actively prepare goods

As mentioned earlier, the first are Toshiba and Fuji Electric, which are investing heavily in capacity expansion.Founded in July 1875, Toshiba, formerly known as Tokyo Chiura Electric Co., Ltd., was formed by the merger of Tokyo Electric Co., Ltd. and Chiura production Co., Ltd. In 1939, Toshiba expected to expand its 8-inch production line in an attempt to create a business line with a monthly production capacity of 150000 pieces, with IGBT as the core. It is proposed that the sales of discrete semiconductor components will reach 200 billion yen in 2021.According to Nikkei, Toshiba will spend about 80 billion yen in the fiscal year ending March 2024 to increase production equipment at its plant in Ishikawa Prefecture, Japan. The group's wafer production capacity will increase from 150000 to 200000 per month. The extra wafers will be delivered to Japanese automakers as well as automakers in China and elsewhere. Toshiba performs well in low-voltage products and can effectively handle voltages of 300 volts or less.

The Tokyo-based company hopes to increase sales in power semiconductors by 30% to 200 billion yen from about 150 billion yen today. It has provided power converters for the power grid.

Prior to this, Fuji Motor issued a medium-term plan for 2023, which shows that the turnover in 2023 is more than 1 trillion yen and the operating profit is 80 billion yen. Fuji Motor will focus on investing in power semiconductors in the future, with an average annual investment of 400-50 billion yen from 2019 to 2023.Fuji Electric said that compared with 2019, the production capacity of the Japanese plant in Yamanashi prefecture will increase by 30% this fiscal year. The company plans to increase production capacity at factories in Malaysia and Japan to enable workers to remove manufactured goods from Japanese-made parts.

Fuji Motor is a pioneer in the development of power semiconductors for cars, and its components have been used by Japanese and other automakers. The company aims to make cars account for half of power semiconductor sales by fiscal 2023, up from 35 per cent in fiscal 2019.In fact, in addition to these two, there are also manufacturers are also actively increasing capacity.Under such an upsurge, Mitsubishi Electric, which has been "pure and abstinent" for many years, has also been moved. Mitsubishi Electric is the second largest manufacturer of power semiconductor type IGBT modules. In recent years, Mitsubishi Electric's investment has shown signs of decreasing. Specifically, Mitsubishi Electric invested 36 billion yen in 2013 and maintained an annual investment level of 100-16.5 billion yen after 2014. But it is worth noting that Mitsubishi Electric invested 55.2 billion yen decisively in 2018, turning to a positive attitude. Its background is the development of the company's SiC power semiconductors.By 2020, Reuters reported that Mitsubishi Electric will invest about 20 billion yen ($187 million) to buy two idle chip factories from Sharp and launch production lines to meet the growing demand for power management chips for electric vehicles. Mitsubishi is a major supplier of such chips to Toyota, and the new plant is scheduled to start operating in November next year and will process wafers for power management chips. Compared with fiscal year 2019, total production capacity in fiscal year 2022 will double.In addition to these manufacturers who are trying to increase production capacity, some manufacturers are increasing their investment in other aspects of power semiconductors.Roma can be said to have used SiC as its main weapon, investing 42.1 billion yen in 2016, 55.9 billion yen in 2017 and 78 billion yen in 2018. Build a new factory in Fukuoka prefecture and introduce a new production line in Miyazaki factory. The goal is to triple the current production capacity by 2021, with a monthly production capacity of 12000 units (6 inches).Within Roma, in fact, some people have put forward the slogan of surpassing Wolfspeed to become the number one in the world in the field of SiC. ROHM expects to invest 250 billion yen over the next three years, and the Shiga Prefecture plant bought from Renesas will also invest in an 8-inch production line.

Aim for gallium nitride

In addition to actively expanding production capacity, in fact, Japanese manufacturers who are deep in power semiconductors have seen a further future-gallium oxide. Data show that gallium oxide (Ga)twoOthree) is a new ultra-wideband gap (UWBG) semiconductor with super-large band gap of 4.8eV.For comparison, the band gap between SiC and GaN is 3.3eV, while silicon only has 1.1eV, which gives the new material higher thermal stability, higher voltage and a natural substrate that can be widely used, allowing developers to easily develop miniaturized, efficient high-power transistors based on this. At the same time, according to the relevant statistics, GatwoOthreeIn theory, the loss is 1max 3000 of silicon, 6 of SiC, and 3 of GaN. With so many advantages, gallium oxide is seen as a more promising technology than gallium nitride.According to the global market forecast of Wide Gap power semiconductor components released by Fuji economy, a market research company, the market size of gallium oxide power components will reach 154.2 billion yen (about 9.276 billion yuan) in 2030, which is larger than that of gallium nitride power components (108.5 billion yen, about 6.51 billion yuan). Although the specific figures have not been released, it can be seen from the market forecast chart below that gallium oxide exceeds gallium nitride at the point in time in 2050.In terms of gallium oxide, Japan leads the world in the research and development of components and substrates. However, it is understood that the research and development of gallium oxide power components is not the current large-and medium-sized power semiconductor enterprises. In other words, it is not Mitsubishi Electric, Fuji Electric, Roma and other enterprises that we are familiar with. But some small businesses.According to the data, the research and development of gallium oxide in the direction of power components in Japan began with the following three people: Mr. Masataka Higashiwaki of the National Research and Development Corporation (NICT), Professor Shizuo Fujita (Shizuo Fujita) of Kyoto University, and Mr. Yurang Kura of Tamura production Institute.Mr. Toshiaki of NICT ended his tenure at an American university and returned to Japan in March 2010 to take gallium oxide power components as a new research and development theme. Professor Fujita of Kyoto University released the research and development results such as gallium oxide deep ultraviolet detection and Schottky Barrier Junction, Epitaxial Growth on sapphire (Sapphire) wafer in 2008, and then devoted himself to the research and development of power components by using the independently developed thin film production technology (Mist CVD method). Mr. Cang you is responsible for the research and development of gallium oxide single crystal wafers in LED direction at Tamura production Institute, and is considering its application in power semiconductors.Their contact with the new energy industry technology comprehensive development organization (NEDO) put forward in 2011 "energy-saving innovative technology development cause-challenge research and development (pre-R & D integrated), super high-voltage gallium oxide power components research and development" this entrusted R & D cause has a certain connection, the entrustment is NICT, Kyoto University, Tamura production Institute and so on. It can be said that this opens the formal research and development of power components.Later, Kyoto University established the venture capital enterprise "FLOSFIA", and NICT Wada Village Studio cooperated to establish the venture capital enterprise "Novel Crystal Technology". Now, both companies are the backbone of gallium oxide research and development in Japan.FLOSFIA was founded in March 2011. different from the epitaxial growth of GaN or SiC in other parts of the world, FLOSFIA researchers have developed a new preparation method, which is the deposition of gallium oxide layer on sapphire substrate to prepare power devices. This mainly depends on a chemical vapor deposition process called "Mist Epitaxy" (spray drying).Novel Crystal Technology (hereinafter referred to as NCT) was founded in 2015, and the scheme adopted by the company is based on Ga grown by HVPE.twoOthreePlanar epitaxial chips, their goal is to accelerate ultra-low loss, low-cost β-GatwoOthreeProduct development of power devices. Develop β-GatwoOthreePower devices.

Now the number of Japanese enterprises participating in R & D continues to increase, and it is showing the scene of "All Japan". Participate in the development of the next generation semiconductor gallium oxide (Ga)twoOthreeThe number of power devices is increasing rapidly. Universities, companies and public research institutions have been involved in gallium oxide (Ga)twoOthree). In addition, investment in development enterprises is taking place one after another.Denso, as a supplier of automotive technology, systems and parts, is also actively laying out GatwoOthreeResearch and development. In January 2018, Denso and FLOSFIA (mentioned above) announced a partnership to invest in and develop a new generation of power semiconductor devices, which is expected to reduce and reduce the energy consumption, cost, size and weight of inverters for electric vehicles.In July 2019, Denso and Toyota jointly announced the formation of a new joint venture. The new company is scheduled to be established in April 2020 to develop the next generation of on-board semiconductor technology. They set their sights on gallium oxide and diamond, power semiconductors that can challenge SiC (silicon carbide) and GaN (gallium nitride). But so far, there have been no new developments about the new company.The United States is also making efforts in this regard. According to foreign media reports, in June this year, the State University of New York at Buffalo (the University at Buffalo) is developing a gallium oxide-based transistor that can withstand a voltage of more than 8000V and is as thin as a piece of paper. It will be used to make smaller and more efficient electronic systems for electric cars, locomotives and airplanes.In addition, researchers at the University of Florida, the United States Naval Research Laboratory and Korea University are also studying gallium oxide MOSFET. Stephen Pearton, a professor of materials science and engineering at the University of Florida, said they were optimistic about the potential of gallium oxide as a MOSFET.In China, although it started late, the research on gallium oxide is also in a state of continuous progress. According to domestic media reports, at the National Science and Technology week held last year, Beijing Gallium Technology Company publicly displayed its gallium oxide embryos, epitaxial wafers and sun-based blind ultraviolet detection array devices.In addition, China Electric 46 Institute has successfully prepared high-quality 4-inch gallium oxide single crystals with a width close to 100mm and a total length of 250mm, which can produce 4-inch, 3-inch and 2-inch wafers. After testing, the crystal has good crystal quality, which will provide strong support for the development of related devices in China.However, Japan said that since it is in Ga,twoOthreeThe leadership of the field, other manufacturers can not pose a threat for the time being.

Said that at the end,

Japan's semiconductor industry has developed for decades, and there are many companies, large and small. But suddenly speaking, I don't seem to be able to name a few. In addition, the "memory" industry, which represents Japan's semiconductor industry, has fallen off a cliff in recent years. In particular, DRAM manufacturers, Japan was ahead of the world in the 1980s and was like a broken kite in 2000. Now you can think of the big Japanese semiconductor manufacturer, only Kioxia (formerly Toshiba).However, Japan still has great advantages in semiconductor materials and equipment. For example, in terms of silicon wafers, several Japanese companies are among the best, and Japan is no less than Japan in terms of gases and compounds used in the production of semiconductor chips. In the case of power semiconductors, Japanese companies not only spend a lot of money to increase production of existing technology products, but also strive to lay out the next generation of power semiconductor materials.Japan's semiconductor strength is not to be underestimated.

* Disclaimer: this article was originally written by the author. The content of the article is the author's personal point of view, semiconductor industry observation is reproduced only to convey a different point of view, does not mean that semiconductor industry observation agrees with or supports this point of view, if there is any objection, please contact semiconductor industry observation.

41019702003041

41019702003041